Cash management isn’t just about tracking pennies — it’s about making every penny work smarter. At its core, it’s the art of collecting, managing, and optimising cash and liquid assets to keep a company running smoothly and financially secure. The goal? Striking the perfect balance to meet obligations, fund operations, and seize new opportunities, all while minimising idle cash and maximising returns.

But great cash management doesn’t exist in isolation. As the business grows, cash management becomes part of a bigger picture — an integrated financial strategy that ties together FP&A, AP/AR automation, capital allocation, risk management, and optimising debt and working capital. When all these pieces work together, connected via integrated processes or APIs, companies can unlock real financial efficiency.

In this article, we will discuss the key factors companies must consider when managing their cash reserves (or “cash float”) and explore the investment strategies and tools businesses can use.

We will also dive into the risks and rewards of these options, helping you make more informed decisions about your company’s financial future.

Let’s get started!

Part 1: How much Cash do you need?

Part 2: Cash Management Explained

Part 3: Cash Management - Risks to Consider

Part one: How much cash at hand do you need?

Let’s dive into what really matters when deciding how much cash a company should keep in its float and reserves. It is not a one-size-fits-all decision, but one that deserves careful consideration and alignment with the company’s Board.

From daily operations to growth strategies, finding the sweet spot for cash reserves is key to staying nimble and secure. Here are the main factors to consider:

Nature of the Business

Operating Expenses: A good rule of thumb is to keep 1 to 3 months of operating costs on hand—think payroll, rent, utilities, and supplier payments.

Revenue Predictability: Is your income steady, like subscription-based businesses, or unpredictable, like seasonal retailers? Predictability often determines how much extra cash you'll need.

Risk Tolerance

Buffer for Uncertainty: A larger cash float acts as a safety net for unexpected—economic downturns, supply chain disruptions, or even natural disasters.

Industry Volatility: If you’re in an industry prone to rapid changes, such as tech or retail, a larger buffer can help you overcome the turbulence.

Liquidity Needs

Working Capital: High operational demands? Keep more cash on hand to stay agile.

Debt Obligations: Ensure you can easily cover short-term debt payments and interest without breaking a sweat.

Economic Conditions

Inflation & Interest Rates: When costs rise or borrowing becomes pricey, having extra cash helps you stay ahead.

Economic Uncertainty: In volatile times, a larger reserve offers stability and peace of mind.

Growth & Investment Goals

Planned Investments: Big moves like acquisitions or capital projects? Make sure you’ve got the cash to back it up.

Unexpected Opportunities: Be ready to act fast—whether that’s acquiring a competitor or jumping on a favourable market shift.

Access to Credit

Credit Lines: If you have strong access to loans or credit, you might not need as much cash in reserves.

Borrowing Costs: When short-term borrowing is expensive, keeping more cash on hand can be a smarter move.

By balancing these factors, companies can maintain cash reserves that support stability, flexibility, and growth.

The goal? Enough cash to stay prepared and seize opportunities without hoarding resources that could go toward driving innovation and success.

General Guidelines

Here’s a quick guide to managing your business’s cash reserves:

Small Businesses: Aim to keep 3–6 months of operating expenses as a cash buffer.

Medium to Large Businesses: Stick to 1–3 months of cash flow or align reserves with your strategic goals.

Highly Volatile Industries: Plan for 6–12 months of expenses to stay ahead of risks.

The sweet spot? It’s all about striking a balance. Keep enough cash on hand to keep things running smoothly, but don’t let excess reserves gather dust—put them to work where they can fuel growth.

Part 2: Cash Management Explained

Every business makes cash decisions regularly - in smaller businesses, it is often a founder/director of the business, and in larger ones - someone in their finance team.

What is Cash Management?

Cash Management is all about making smart decisions — timing critical payments and managing cash holdings effectively. By doing so, you can maximise the use of your available cash while reducing financial risks and keeping your finances running smoothly.

Horizon: Usually up to 30, sometimes up to 90 days

Frequency: Daily or weekly

Tools you need: Access to bank accounts and cash payments and collections.

Connected processes: Cash forecasting, Accounts Payable & Spend Management, Accounts Receivable and Credit controls, FX management.

What’s new in Cash Management?

Open Banking feeds make real-time cash management real. No more daily chores to log into multiple bank accounts, collate balances in spreadsheets and reconcile discrepancies. Automated solutions such as HedgeFlows Cash Management help get real-time visibility and easily track down any variances.

Easier access to bank accounts via account aggregators makes access to the best deposit deals on the market simpler. They also can be a useful tool in diversification strategy to avoid the bank credit risk akin to the Silicon Valley Bank crisis.

Solutions such as Wise Interest make access to money market funds easier. TreasurySpring offers innovative investment instruments to larger corporates.

Cash Management Strategies

Business Bank accounts

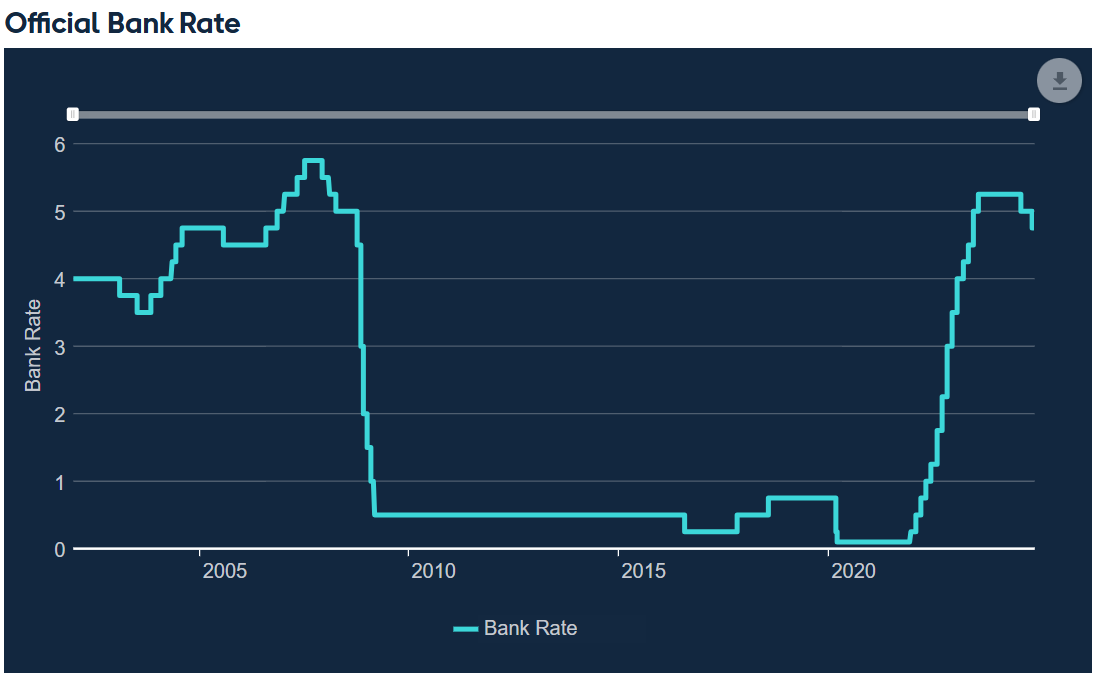

For most companies, the go-to tool for managing cash is a simple business bank account. It offers quick access to funds for daily operations and can even integrate with finance and operations systems. Sounds convenient, right? The downside: most business accounts offer little to no interest on your money.

For years, this wasn't a big deal. Between 2009 and mid-2022, the Bank of England’s Official Bank Rate sat between 0% and 1%, meaning the opportunity cost of keeping cash in these accounts was virtually nonexistent. But times have changed, and it might be time to rethink where your money works best!

During the 2023-24 period, interest rates have climbed to normal, but many businesses are still missing out. Imagine this: a mid-sized company with a £10 million turnover, keeping an average balance of £1.5 million in a business bank account, could lose over £60,000 annually in interest. That’s money left on the table!

The key takeaway? Don’t let your hard-earned cash sit idle. Minimise those overnight balances in low-yield business accounts and make your money work harder for you.

Sweep facilities & pre-programmed payments

One effective way to maximise returns on your cash balances is to use a sweeping mechanism that automatically transfers funds overnight into interest-bearing accounts and schedules payments to current accounts when needed. While many banks offer this service, the interest rates are often low, and automated sweeps are usually limited to accounts within the same provider.

That’s where companies with advanced finance systems, like HedgeFlows, stand out. They can set up programmatic sweeps without these limitations, giving you access to a broader range of options, including bank accounts, money market funds and T-Bills—all without adding extra workload for your finance team. It's a smarter, more flexible way to make your money work harder.

Term deposits

The interest rate you earn on your cash balances doesn’t just depend on the account—it also depends on the “term,” or how long you commit to keeping your money in that account. Term accounts, Fixed Term Deposits, or Certificates of Deposit (CDs) typically offer higher returns than instant access accounts. Even locking your funds away for as little as one month can significantly boost your earnings.

For companies, opting for longer terms often provides better returns, as banks benefit from longer-term deposits in terms of regulations. However, there can be exceptions. If central banks are expected to slash interest rates, shorter terms might actually offer better returns.

This strategy does require some cash flow forecasting to ensure you won’t need access to the funds before the term ends. Keep in mind that most term accounts won’t allow early withdrawals. But with a little planning, term accounts can help maximise your returns and put your idle cash to work!

Notice accounts

A variant of term accounts is notice accounts, where the cash deposited can only be accessed upon giving notice (typically 30, 60, or 90 days). With some notice accounts, access without notice may be permitted but with a penalty of foregoing interest for the period. This way, the company can access the cash in an emergency at short notice.

Short-term money market funds

Money market funds are smart, cash-like investments that combine safety with income potential. They hold a mix of high-quality bonds set to mature within a year, giving you a low-risk way to put your cash to work. Short-term funds are ultra-low risk, while standard money market funds offer slightly more risk for potentially higher returns. Fund managers focus on safety by maintaining a portfolio of short-maturity, top-tier bonds. These funds are not only affordable but also easy to buy and sell, making them a flexible, cost-effective way to manage your cash. However, it’s important to note that money market funds differ from traditional bank accounts — learn more in the Risk to consider section below!

Treasury Bills (T-Bills)

Short-term government bonds, known as T-Bills, offer a simple and secure way to invest with maturities ranging from just a few days to a year. They’re highly liquid and come with extremely low risk — after all, it’s nearly impossible for a government to default on debt in its own currency (it can always print more!).

T-Bills pay interest rates determined by the market, and their prices fluctuate daily. If you hold a T-Bill until maturity, the interest rate is locked in and known from the start. Need cash earlier? No problem! You can sell your T-Bill on the market anytime. Just keep in mind the interest rate you earn will depend on market conditions at the time. Flexible, low-risk, and easy to trade — T-Bills are a reliable option for short-term investing.

Commercial Paper (CP)

These are similar to T-Bills i.e. short-term debt instruments, but issued by companies with high credit ratings rather than the government, and so provide slightly higher interest rates than T-bills.

Collateralised loans (“repurchase agreements”)

New providers such as TreasurySpring have recently introduced innovative financial products that give companies access to other financial instruments. One such product is a collateralised loan, where a company provides a short-term loan to a bank (similar to making a deposit). The twist? This loan is backed by collateral, such as a government bond or T-Bill, making it seem like a safe option for earning extra interest beyond simply purchasing a T-Bill. It’s all documented through specialised standard agreements known as “repurchase agreements.” While this approach appears low-risk in theory, it comes with additional risks that aren't always obvious. Companies must look closely and carefully evaluate these potential pitfalls before diving in. These are discussed below.

Structured deposits

Some banks offer higher-risk deposit products that use derivatives to enhance interest rates. These boosted rates depend on specific movements in financial asset prices, such as FX rates, interest rates, stock markets, or commodity prices. While the potential returns can be enticing, these products carry significant risk and are best suited for sophisticated finance teams. To stay on the safe side, ensure your rationale aligns with your company’s risk appetite and is well-documented to avoid the perception of speculative investing.

Part 3: Cash Management - RiskS TO CONSIDER

Every financial decision comes with its risks, and cash management is no different. Let’s take a look at two key risks you should keep in mind:

1. Type of institution

Banks

Although a highly regulated industry, banks vary in their riskiness. This is reflected in the credit ratings assigned by rating agencies such as Moody’s and Standard & Poor, in bank bond prices observed in the publicly traded bond markets and can also be reflected in the interest rates banks offer on their deposits. Occasionally, banks fail. Over the course of five days in March 2023, three small-to-mid-size U.S. banks failed, causing the US government to intervene in various ways.

Non-banks

These include governments and other non-bank companies who can issue many of the instruments described in the prior section (T-Bills, bonds, commercial paper). Governments are the least risky and other companies depend on the sector. Many large companies have credit ratings that are better than banks.

2. Direct vs indirect ownership

When you deposit money in a bank or buy a debt instrument such as a T-Bill or commercial paper, you enter into a direct legal relationship with the entity to which you are giving your cash.

When you buy a money market fund or enter into a structure such as the collateralised repurchase agreement described above, you are entering into a contract with a holding entity which then pools your money with those of others and buys and holds interest-bearing assets on your behalf. Thus, you have an indirect relationship with those to whom you have entrusted your cash. In times of financial turmoil, it can be more difficult to access your cash as arrangements will need to be unwound and assets sold by the holding entity. The holding entity may find it difficult to do this, and there could be a delay in receiving your money or in the worst case, it could become encumbered as part of a dispute.

It is for this reason that the Bank of England warns that in times of market panic and a rush to cash, there may be liquidity issues in money market funds and other similar structures.

Risk reduction strategies

It is possible to mitigate the risks described above in various ways. As with all risk management, best practice suggests that the aims and relevant metrics should be decided in advance and documented as part of the finance strategy.

Financial Services Compensation Scheme (FSCS)

The government protects most companies’ deposits in banks, building societies and credit unions up to £85,000 per deposit taking institution via the Financial Services Compensation Scheme. Certain sectors (such as most type of regulated financial services companies) are excluded.

The £85,000 limit is modest compared to other countries (the US provides similar FDIC coverage for up to $250,000). And for sole traders, the £85,000 limit may include your personal accounts with the same bank.

Using FSCS to mitigate risk

Although the FSCS effectively provides a government guarantee for bank deposits, it does so only up to the £85,000 limit per bank. So, a natural way to increase coverage would be to spread deposits across different banks thus multiplying the limit. Although this sounds appealing, it can become difficult to track and manage accounts across multiple banks. And for many smaller companies, this added complexity may not seem worthwhile.

Diversification and interest rate optimisation

Once cash balances get above a few hundred thousand Pounds it becomes impractical to spread cash around multiple providers to remain fully covered by the FSCS. Instead, companies may choose to reduce risk by diversifying their cash balances across different providers even if each balance is in excess of the FSCS limit. This is where careful consideration of a bank’s risk profile becomes important and third-party analysis such as reports by credit rating agencies may be considered. Typically, a finance team would need to balance the riskiness of a bank with the interest rates offered. There will generally be a trade-off between bank risk and interest rate optimisation, with smaller, newer or non-UK headquartered banks generally offering higher rates.

Other non-bank providers also have a part to play when diversifying risk and optimising yield, whether money market funds, T-Bills or Commercial Paper.

Account aggregators

Maximising the FSCS limit, diversifying bank risk and optimising the yield received on cash typically requires dealing with multiple banks, which can be both an initial and ongoing hassle given most bank onboarding processes. Another option is to use account aggregators. These providers allow you to access accounts at dozens of banks and building societies with a single onboarding process and to move money easily between them. This can provide a convenient way to open and maintain accounts at a large number of banks and transfer funds between them.

Summary

Here’s a quick rundown of key points to keep in mind:

- Cash management isn’t just about crunching numbers – it’s a core part of your finance strategy. Tightly linked with cash flow forecasting, it becomes a breeze with strong processes and a powerful finance platform like HedgeFlows.

- Set clear parameters, risk appetite, and target yields for managing cash. This should be a collaborative effort between the finance team and the Board, tying into broader discussions around risk.

- Choosing the right cash management products comes down to a few key factors:

- When will you need access to the funds?

- Are you working with a bank or a non-bank institution?

- What type of product suits your needs – direct or indirect ownership?

- How do you balance risk against interest rates?

- Stay on top of your cash strategy. Regularly monitor rates and risks, and adjust as needed to ensure you stay within your defined risk appetite while taking advantage of any mitigation measures.

Smart cash management is all about planning ahead, staying flexible, and keeping your goals aligned.

A summary table of products with their characteristics and risks is given below:

Table: Cash Investment Alternatives and Risks

|

Product |

Provider |

Ownership |

FSCS |

Risk |

|

Business Bank Account |

Bank |

Direct |

Yes |

Low (almost none if covered by FSCS) |

|

Term deposit account |

Bank |

Direct |

Yes |

Low (almost none if covered by FSCS) |

|

Notice account |

Bank |

Direct |

Yes |

Low (almost none if covered by FSCS) |

|

T-Bill |

Government |

Direct |

No |

Extremely low |

|

Money market fund |

Non-bank |

Indirect |

No |

Low/Medium |

|

Commercial Paper |

Non-bank |

Indirect |

No |

Medium |

|

Repurchase Agreement |

Non-bank |

Indirect |

No |

Medium |

|

Structured Deposits |

Bank |

Direct |

No |

High |

If you have any questions about managing your cash and currencies, please get in touch or schedule a call with our team: