New business models, from companies such as TransferWise and Revolut, have transformed the cross-border payments market over the last 5 years. They have thrust greater transparency onto the fees charged for foreign currency payments. Retail clients can now exchange and transfer currencies faster and cheaper from anywhere in the world. Although some entrepreneurs and small businesses have benefited from this innovation, a tremendous gap remains between the products and services they receive from their banks or FX brokers and what their larger business competitors receive from Corporate Banking divisions.

Currency Risks from B2B cross-border payments

Anyone who has traded goods and services internationally knows that cross-border trade is complex and payments are far more involved than for retail commerce. Most cross-border commerce remains business-to-business (B2B), and over 60% of such transactions in Western Europe are made on Open Account terms - where the buyer is obliged to pay the seller a pre-agreed number of days after being invoiced.

As a consequence, from the moment the foreign currency invoice is booked and until it is paid, the business has to absorb moves in foreign currency exchange rates. For example, a British buyer paying a French supplier could suffer unnecessary costs if the Euro appreciates against Pound Sterling. Such a loss would show up as a foreign exchange loss in their income statement unless they are able to protect themselves against this risk. Whether exchange rates are simply satisfactory or offer an attractive opportunity to buy or sell abroad with greater margins, waiting to convert at a payment date can result in opportunity costs.

Average 45 days of wait in UK B2B trade

Most small businesses, whether dealing with their high-street banks or neobanks, will have to wait until the payment date to convert foreign currencies. They can avoid this if they have foreign currency accounts and have the spare working capital to buy and hold cash balances in multiple currencies. However, this is highly inefficient for most small businesses and constrains their ability to grow. Much can change in the currency world over a 45 day period and unexpected currency losses are often the result; 67% of small and medium-sized businesses (SMEs) surveyed by Bibby Financial Services in 2017 said they were adversely affected by the currency moves.

It is common practice for larger businesses to mitigate these risks. A Barclays survey found that 71% of multinational companies with a turnover under £1bn hedged their currency risks. For those with a turnover over £1bn this figure rose to 86%.

Unfortunately, most SMEs rarely have the tools to estimate how much risk they take due to currency movements. Even when they know and understand the risks,and choose to mitigate them, they lack easy access to affordable products to do so.

An easy way to estimate FX risks

HedgeFlows’ FX risk analyzer tool is a unique product for SMEs. It allows anyone to estimate the uncertainty that arises from not knowing the FX rate on the day when foreign cashflows will be exchanged.

HedgeFlows uses historical data from the Bank of England to calculate a hypothetical impact from foreign currency risk (due to currency rate changes between invoice and payment dates) so mimicking a client's trade contract. In financial markets history has often served as a good starting point to predict the future; similarly, HedgeFlows' FX risk analyzer tool can look at what happened to exchange rates over similar periods in the past to give a prediction for future risk.

Over very short periods of a few days, currency moves are relatively tame and are of little concern to most businesses. However, it is important to estimate how far a currency could move should worst case scenarios repeat themselves, especially when geopolitical situations are on the horizon.

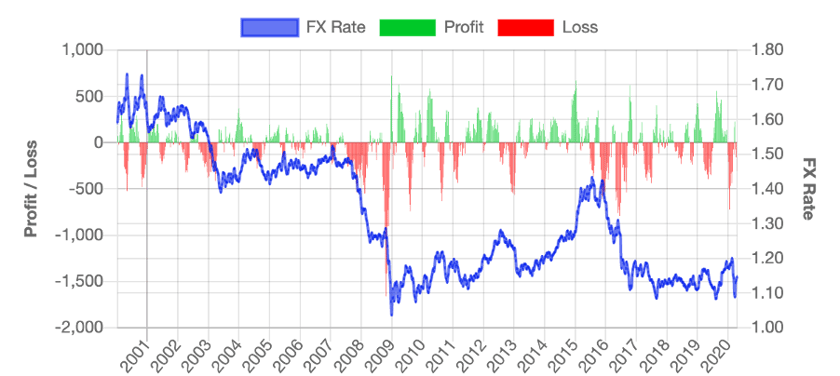

For example, in our scenario of a Euro payment by British buyers, we are interested in how much more the payment would cost in extreme cases. In the worst case, such as in 2009, the payment would have cost almost 20% more. Furthermore, for every one in five past cases the payment lost 3% or more. If a small business wishes to avoid a 3% or greater loss in margins, it should evaluate the option of fixing its currency rates now to avoid such a loss:

GBP/EUR FX Rate and Historical Profit & Loss in GBP

EUR 10,000 payable in 45 days

Most of the time currency moves over shorter periods are relatively tame and would cause little concerns to most businesses. It is important however to estimate how far the currency could move should less frequent scenarios repeat themselves, especially when similar situations are on a horizon.

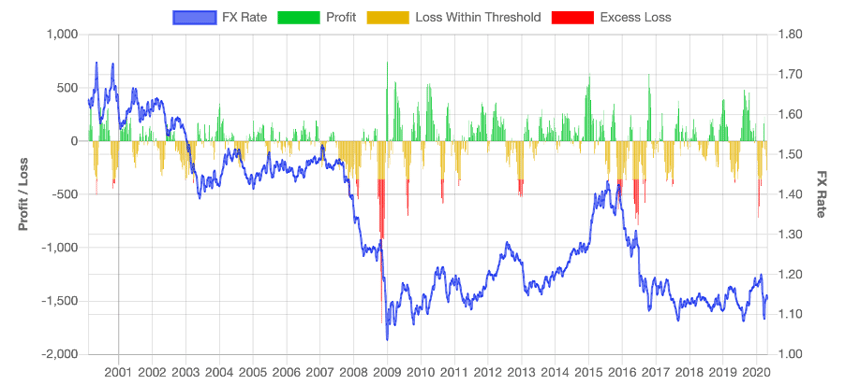

For instance, in our case of EUR payment by British buyers, we are interested how much more the payment can cost in extreme cases. It turns out that in the worst case (in 2009) such payment costed almost 20% more, and on one in five occasions in the past, such payment could lose 3% or more. If 3% loss is a concern for your own business margins, you can see when such moves happened in the past and evaluate if it likely to happen again:

GBP/EUR FX Rate and Historical Profit & Loss and Excess Loss in GBP

EUR 10,000 payable in 45 days