Whenever you do business with overseas suppliers or buyers, you will likely buy or sell goods or services in foreign currencies. Such foreign invoices and payments usually result in a real financial impact on your business that accounting systems report in the form of foreign currency gains or losses. Such effect can come from both exchange rate fluctuations and, surprising to many, fees charged by your bank or payments provider for currency conversions. This article explains the primary sources of foreign exchange gains and losses and the best ways to manage them.

Foreign currency conversion fees in your gain or losses

Foreign currency conversion fees are one of the most overlooked reasons behind your currency gains and losses.

When your bank or payments provider, such as PayPal or WorldFirst, converts currencies for your foreign payments, they will charge a foreign conversion fee. This fee usually means that your provider will charge you a margin to sell you a given foreign currency amount than it costs them in the wholesale market. While many fintech companies such as HedgeFlows or Wise are upfront about such costs, most incumbent banks or payments providers are often less transparent. They include their conversion charges in their quoted exchange rates.

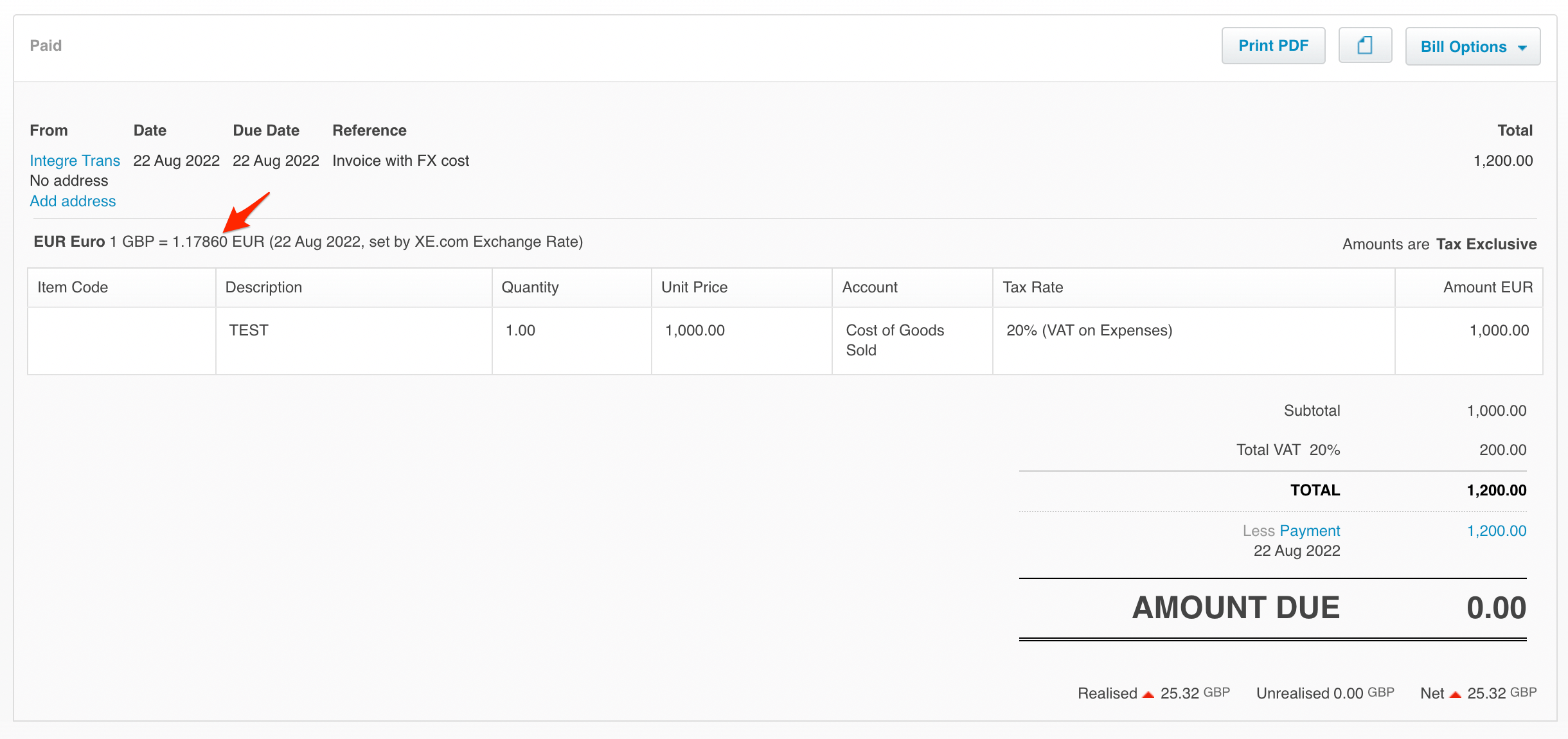

Most popular accounting systems, such as Xero, will record the cost of currency conversions as part of Foreign Currency Gains and Losses. Accruing a bill or invoice in foreign currency in Xero will take by default the exchange rates from XE.com in the case of Xero (1.1786 in the example below):

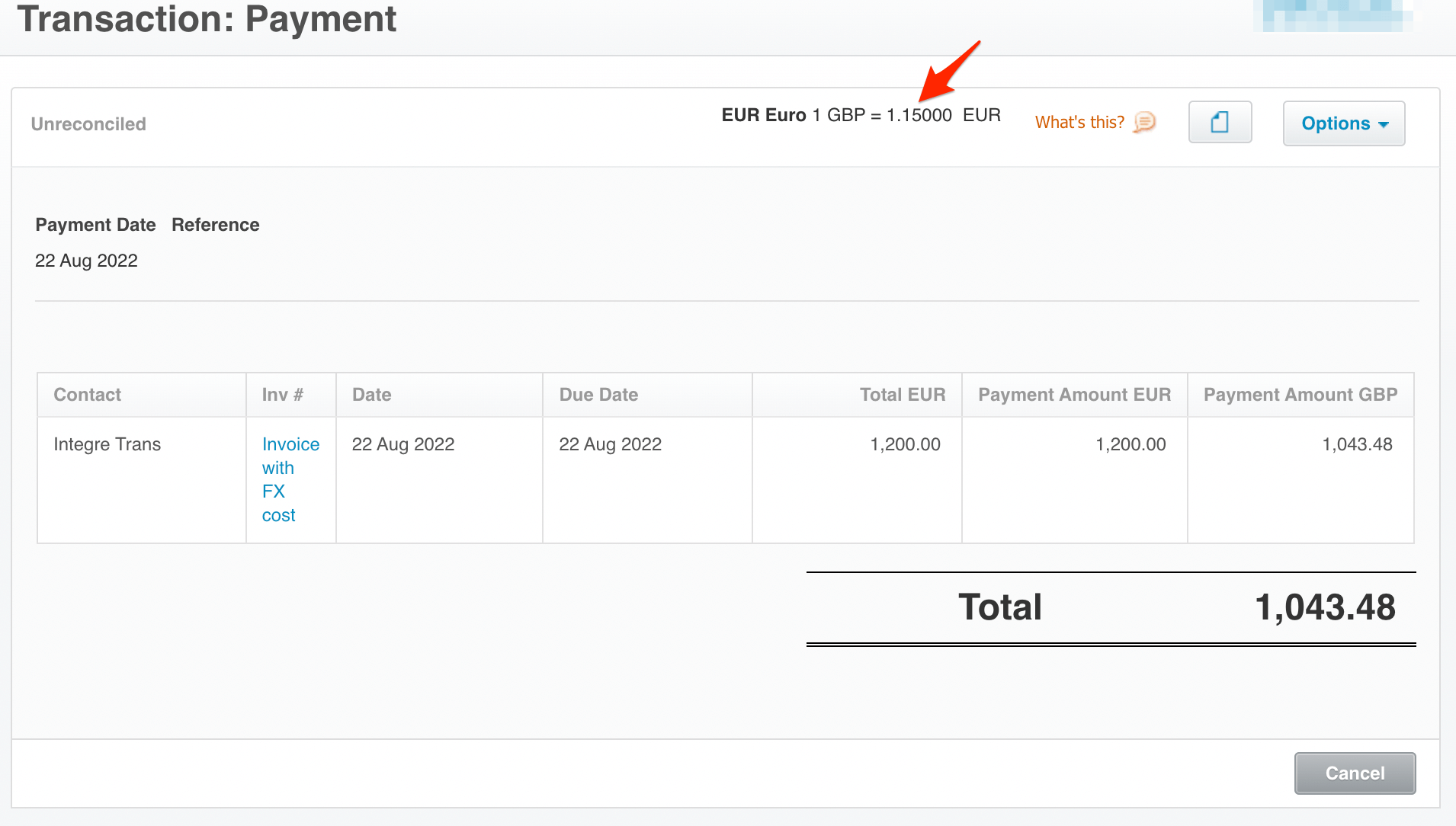

When such a foreign currency invoice is then paid from your home currency account via a currency conversion, Xero payments are processed using the real exchange rates (1.1500 in the example). This happens even if you accrue and pay the invoice on the same day; you will have two exchange rates recorded:

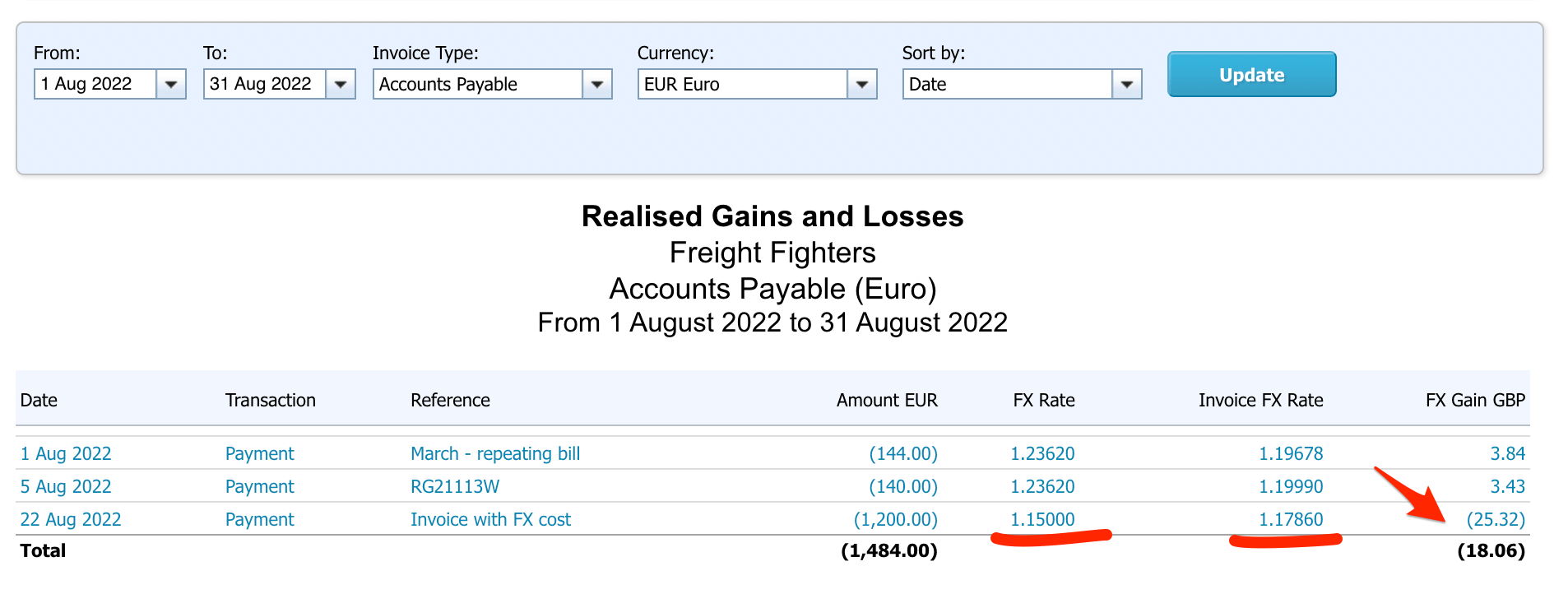

The resulting difference is then recorded in Realised Gain and Losses and has a direct impact on your business income:

Invoice payments with credit terms and resulting FX gains and losses

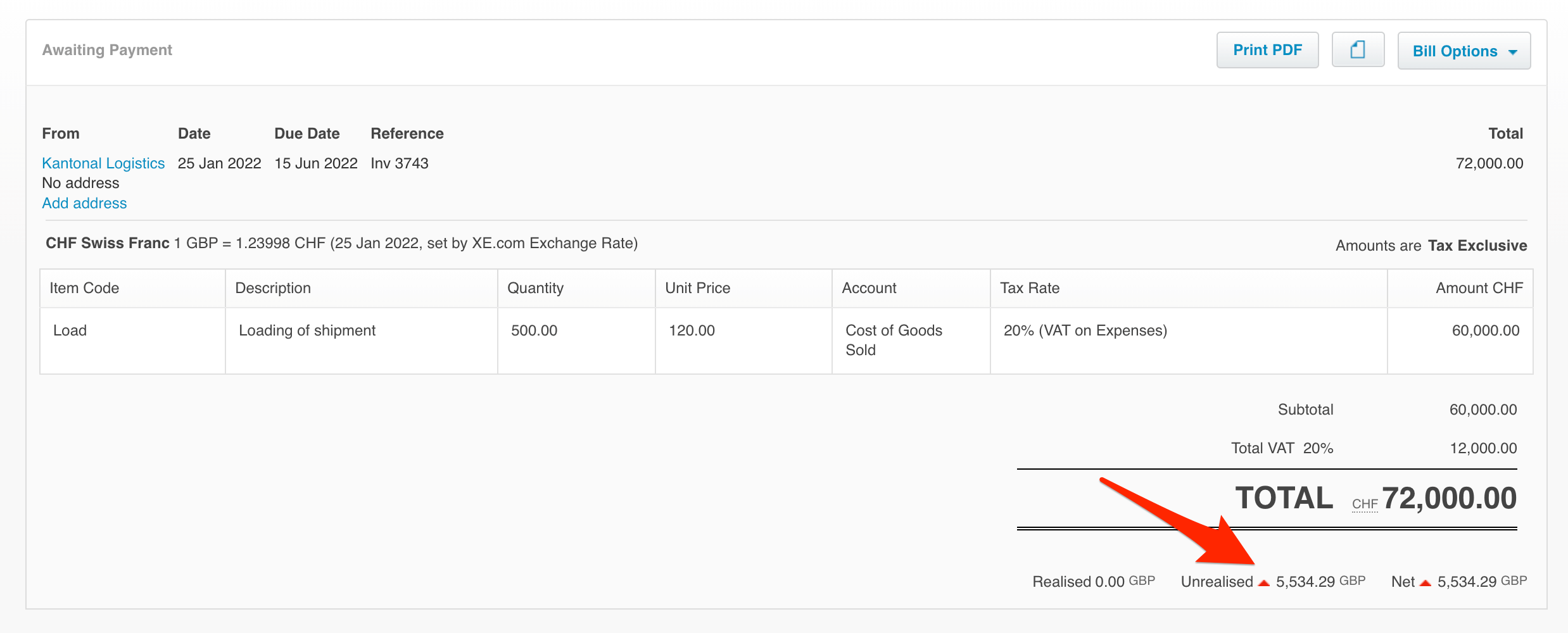

Most Business-to-Business (B2B) trade happens on account (such as 30-day credit terms), and the lag between the invoicing and payment dates often results in a currency impact as foreign exchange rates fluctuate. An average business invoice in the UK takes approximately 45 days to be paid, during which the exchange rate between Pounds Sterling and Euro or US Dollar can easily move 2-3%, for example. In such case, the impact of exchange rates can be seen even before one pays a foreign invoice - as an unrealised gains & loss on an individual invoice in Xero or in the Unrealised gains and losses section on P&L:

What happens when you pay your foreign currency bill in Xero?

When you pay a foreign currency in Xero, it will calculate the realised Foreign currency gain & loss by comparing the rate when the invoice was issued with the one when it was paid. As a result, when you combine payment with a foreign conversion, Xero includes any additional foreign exchange charges from your provider with the impact of currency fluctuations. If you send your foreign transfer from your foreign currency account, the foreign currency gains and losses are affected by currency fluctuations only.

HedgeFlows automated tools to explain FX Gains & Losses

HedgeFlows users can benefit from automated reports thanks to our FX Gains & Losses explainer. Read more here or schedule a demo call with our team.

How to reduce your exchange losses

-

Control your exchange costs by finding a provider with low, transparent foreign exchange charges.

-

Book foreign exchange for accrued invoices in advance when exchange rates work for your margins

-

Use multi-currency accounts to manage currency balances and consider managing your currency risks.

If you use Xero for your international payments and transactions, HedgeFlows offers the perfect integration; multicurrency transactions (international bulk payments and collections), automated reconciliations and more.

Get in touch if you'd like to know more about HedgeFlows and how it works with Xero.